For years, insurance growth strategies have been built on a simple assumption:

More quote requests create more opportunities to sell policies.

On the surface, the logic makes sense. If agents speak with more consumers, sales should follow. As a result, many acquisition programs still evaluate performance marketing partners primarily on quote volume: calls delivered, leads received, or forms completed.

But inside the sales operation, a different reality often emerges.

Beyond a certain threshold, increasing quote volume doesn’t necessarily improve results. Instead, an oversaturated volume can actually reduce close rates, increase agent burnout, and raise the true cost per policy.

What looks like a marketing success on the front end often becomes an operational constraint on the back end.

This is why organizations like Soleo increasingly view performance marketing not just as a traffic problem, but as a sales-efficiency problem.

Why Quote Volume Became the Default Success Metric

Quote volume became the dominant KPI for understandable reasons: it’s easy to measure, easy to report, and fits cleanly into traditional CPL and pay-per-call pricing models.

Historically, lead generation solved a simple challenge: agents needed more conversations.

But today, the insurance marketplace has changed:

- Consumers research more before calling

- Compliance requirements extend call handling time

- Policies are more complex

- Acquisition costs are higher

- Sales conversations require more consultative engagement

The constraint is no longer simply getting calls – it’s turning those calls into policies efficiently.

The Multi-Buyer Lead Problem: When One Quote Becomes Many

Another hidden driver of inflated quote volume is the structure of lead distribution itself.

Not all performance marketing partners sell exclusive leads or calls. Many leads are distributed to multiple buyers either simultaneously or sequentially. From the supplier’s perspective, this increases the value of each consumer inquiry, but from the carrier or agency perspective, this model can lead to issues.

Under this model, the same consumer may receive multiple calls within minutes, already be deep in a competitor’s quoting process, and become frustrated with repeated outreach.

When one consumer enters multiple sales funnels at once, quote volume rises but the probability of any single agent closing the sale falls.

Importantly, this isn’t simply a vendor issue. It’s a measurement issue.

If partners are evaluated primarily on lead delivery counts, the system naturally rewards distributable volume. However, if partners are evaluated on backend policy outcomes, the system naturally rewards consumer intent and fit.

The Operational Reality Inside the Call Center

Even with strong lead sourcing, agent capacity is finite.

Every inbound quote consumes agent time, needs analysis, quote generation, and follow-up handling. When quote flow exceeds realistic handling capacity, performance is unable to scale.

Finite Bandwidth

Higher inbound volume means less time per consumer, which leads to less discovery, personalization, and consultative selling.

Queue Pressure Changes Behavior

When calls stack up, conversations become transactional rather than advisory.

Lead Fatigue and Cherry-Picking

Over time, agents recognize patterns in which leads tend to convert, and they may unconsciously disengage from lower-intent prospects, creating inconsistent performance across the team and lowering overall morale.

The Hidden Performance Costs of Too Many Low-Intent Quotes

Excess quote volume reduces efficiency, and businesses can measure the downstream impact.

Organizations often see:

- Lower close rates per conversation

- Higher cost per policy written

- Increased short-duration calls

- Higher abandonment rates

- Worse consumer experience

Why Backend Conversions Matter More Than Frontend Volume

This is why more insurance organizations are shifting how they evaluate acquisition partners.

Instead of asking, “how many quotes did we receive?”, they’re asking:

- How many policies were written?

- What revenue did those policies generate?

- What was the cost per issued policy?

- Which traffic sources consistently convert?

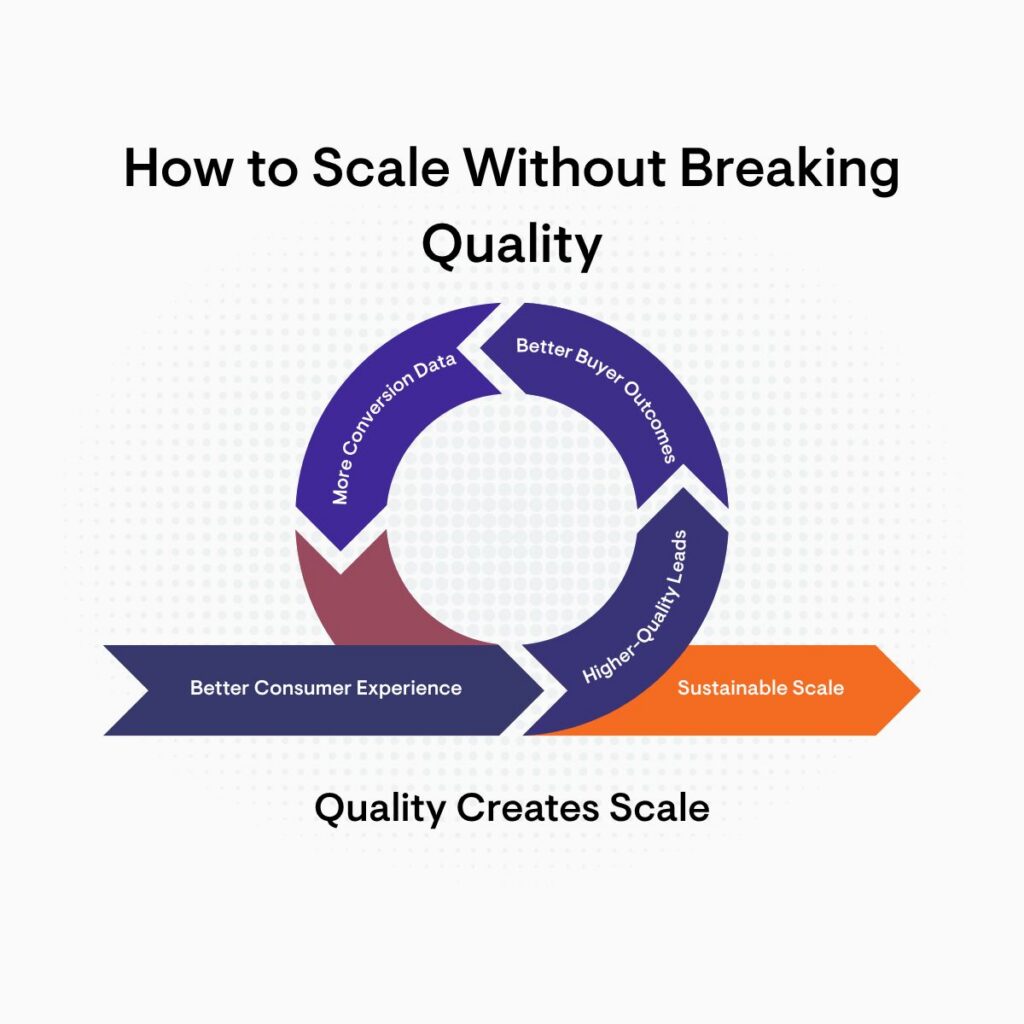

When conversion feedback flows back into marketing optimization, traffic sources can be refined, consumer targeting improves, low-intent segments naturally filter out, and agent productivity stabilizes.

In this model, volume becomes the result of strong performance — not the primary objective.

What High-Performing Insurance Programs Do Differently

Organizations achieving consistent acquisition efficiency tend to:

- Share downstream conversion data with marketing partners

- Evaluate partners on issued policies, not just delivered leads

- Prioritize consumer intent signals over raw volume

- Optimize toward revenue per call, not calls per day

In these environments, performance marketing functions less like a traffic faucet and more like a calibrated extension of the sales organization.

The companies that outperform their competitors are aligning acquisition strategy with agent capacity, consumer intent, and measurable backend outcomes.

Because ultimately, the goal isn’t more quotes – it’s more policies sold.